Web Content Viewer Header SGK

Actions

Actions

- ${title}

- Minister

- Introduction of the President of Institution

- Objectives and Duties of SSI

- History

- Organization Chart

- Social Security System

- Short Term Insurance Branches

- Long Term Insurance Branches

- Universal Health Insurance

- E-book on Universal Health Insurance System in Turkey

- E-book on the Organizational Profile of SGK & Social Security System in Turkey

- I Want To Make Crediting For My Foreign Services

- Foreign Pension Transactions

- Social Security Agreements

- Foreign Healthcare Transactions

- Social Security Rights in the Process of Membership to European Union

- On-going Projects and Activities Made During the Process of Social Security Reform

- ISSA (International Social Security Association)

- Statistics

- Basic Indicators of Monthly Social Security

- Monthly Statistical Information

- Monthly Statistical Bulletins

- Useful Links

- Contact Us

Web Content Viewer Content SGK

Actions

- ${title}

Long Term Insurance Branches

Long Term Insurance Branches

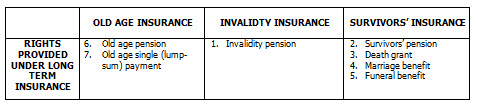

Long term insurance branches include the services relating to invalidity, old-age and survivors’ benefits.

1. Old-Age Insurance

Old age insurance is a mandatory and contributory social insurance that allows insurance holders to have an old age pension when they reach a specific age. Old age pension and old age single payment are the rights provided under this type of insurance.

a) Old age pension

For the individuals who are deemed to be insured according to the Law No: 5510 for the first time; old - age pension shall be granted provided that the individual is over 58 if the individual is woman or over 60 if the individual is male and that minimum 9000 days of invalidity, old - age and survivors insurance premiums are notified. However, the conditions necessary to receive old age pension have softened for the insurance holders working on service contract. The number of premium days shall be applied as 7200 premium days for these insurance holders at the above-mentioned ages.

It is envisaged that the age condition stated in Law No: 5510 shall be raised to 65 gradually starting from 2036 until 2048 for both male and female insurance holders.

Apart from specified in the law by general regulations, there are some special arrangements brought into use of older aged pensioners, those who cannot benefit from the invalidity pension due to the existing disability during his/her first work, the severely disabled, mineworkers and those with early ageing disease. Based on these arrangements, the insurance holders can receive old age pension provided that minimum 5400 days of invalidity, old - age and survivors insurance premiums are notified and 3 years are added to the above –mentioned age limits without exceeding the age of 65.

The Law stipulates different conditions for awarding old age pension to some exceptional insurance holders who became invalid at the starting date of working, whose invalidity rate between 40% and 59%, mineworkers and those with early ageing disease.

In case the female insurance holders with an invalid child permanently in need of another person request for retirement or old-age pension, one fourth of premium days paid after the effective date of the Law shall be added to the total number of premium days and the added days shall be deducted from the age limit of retirement.

b) Old age single (lump-sum) payment and revival

Among the insurance holders working on service contract and working on their own names and accounts and the individuals who become insurance holders for the first time under civil servant status pursuant to the Law No: 5510, the insurance holders, who quits work or closes workplace for whatsoever reason and who does not have the right to receive invalidity and old -age pension although the age condition for receiving old-age pension is met, shall receive the sum of invalidity, old -age and survivors’ insurance premiums of each year paid for those working on their own names and accounts and notified for the name of those working on service contract and civil servants as single payment, being updated with the update coefficient realized each year, for the years from the year of the premium up to the date of written request.

In case the individuals whose services are eliminated by making single payment in accordance with the Law No:5510 and whose invalidity, old - age and survivors’ insurance premiums are notified by again being subject to this Law submit a written application,- provided that they pay the amount, found by updating with the update coefficient realized each year for the years between the date of single payment and the date of written request, by the end of the month following the date of notification of such to the concerned party- these services shall be revived and considered in the execution of this Law.

2. Invalidity Insurance

The invalidity insurance is a mandatory social insurance with premiums that allows insurance holders to have invalidity pension provided that the status of invalidity is determined and certain conditions, are met.

a) Invalidity pension

In case the insurance holders who are subject to service contract and those subject to work on their own names and accounts and civil servants are determined to have lost working power or earning power in profession minimum at 60% or at a degree which does not allow him/her to carry out his/her duties due to work accident or occupational disease by Health Committee of the Institution as a result of reviewing the reports and the medical documents prepared duly by the healthcare service providers authorized by the Institution upon request of insurance holders or employers, they shall be deemed to be invalid. However, if it is determined in advance or afterwards that the insurance holder has lost 60% of the working power or earning power in profession at a degree not to allow him/her to carry out his/her duties before the date of first start to work under insurance, then the insurance holder shall not benefit from invalidity pension due to such disease or handicap.

In order to put an insurance holder on invalidity pension, the insurance holder should;

- be deemed to be disabled as per the Law No. 5510

- be holding insurance for a period of minimum ten years and should have paid totally 1800 days or in case the insurance holder is disabled to the extent of being in need of permanent care of another person, should have notified 1800 days of invalidity, old -age or survivors’ insurance premiums, without seeking any insurance period,

- have submitted a written request to the Institution after quitting the work he/she was working under insurance or closing or transferring the workplace due to his/her invalidity. However, it is obligatory that the individuals who work on their own names and accounts should have paid entire premiums or any kind of debts related with premiums, including the universal health insurance.

3. Survivors’ Insurance

The insurance holders’ death poses a social danger for their relatives he/she had been looking after and left behind. One of the long term insurance branches, the survivors’ insurance is a compulsory and contributory insurance branch which provides a monthly pension to survivors including spouse, children and parents in case the insurance holders deceased due to a reason other than work accident and occupational diseases. The rights provided under survivors’ insurance are survivors’ pension, death grant, marriage allowance for the girls who are receiving monthly pension and funeral allowance.

a) Survivors’ pension

Survivors’ pension shall be payable to the right holders upon written request in case;

- minimum 1800 days of invalidity, old age and survivors’ premiums are notified or there is an insurance status of minimum 5 years, excluding any kind of debt periods, and totally 900 days of invalidity, old - age and survivors’ premiums are paid for the insurance holders working on service contract,

- the individuals suffering from war invalidity or duty disability are entitled to invalidity, duty disability or old - age pension while already receiving invalidity, duty disability or old - age pension, however the relevant process is not completed,

- the invalidity, duty disability or old - age pensions were terminated due to the fact that the pensioner had started to work as insured.

However, in order to award pension to the right holders of individuals working on his/her own names and accounts it is obligatory that the entire premium or any kind of debts related premiums, including the universal health insurance, should be paid.

Of the pension to be calculated for the deceased insurance holder in accordance with the Law No. 5510;

a) 50% shall be payable to the widow spouse; and 75% to the childless widow spouse, who is put on pension, in case such individual is not put on income or pension due to working under this Law or under legislation of a foreign country or due to her own insurance status,

b) Among the children, who are not put on income or pension due to working under this Law or under legislation of a foreign country or due to their own insurance status;

- the ones who have not completed the age of 18, the age of 20 in case receiving education in high school or equivalent, or the age of 25 in case receiving higher education; or whose insurance premiums are notified or

- the ones who are found to be disabled by losing minimum 60% of working power based on the decision of Health Committee of the Institution; or

- the daughters, whatever the ages are, not married, divorced or widow,shall receive 25% each.

c) If there are shares left over from spouse and children who are right holders, 25% totally to mother and father, provided that the figure is less than the net amount of the minimum wage of the income obtained from any kind of earnings and revenue and that they are not put on income and/or pension excluding the income and pension rights granted due to other children; if the mother and father is over 65 years of age, they shall be entitled to totally 25%, under the above conditions, without considering the left over share,

d) 50% shall be payable to each of the children stated in item (b), who are left both motherless and fatherless or suffer such status at a later date due to death of insurance holder; whose mothers and fathers do not have marriage connection or whose fathers and mothers have marriage connection at the time of decease but mother or father is married later on and the ones who are the sole right holders receiving pension.

Children who are adopted or recognized or whose lineage connection is corrected or fatherhood is ruled on, and the children of the insurance holder born after decease shall benefit from the pension under the abovementioned principles.

The total of the pensions payable to the right holders cannot exceed the amount of the pension of an insurance holder. If necessary, proportional reductions shall be applied to the pensions of the right holders in order to observe this limit.

b) Death Grant and Revival

In case the right holders of the deceased insurance holders, who work on service contract and on their own names and accounts and who became civil servants for the first time pursuant to the Law No. 5510 are not put on survivors pension, the amount calculated as per the Law No. 5510, shall be payable to the right holders in single payment, considering the provisions of this Law and taking the date of decease as basis.

c) Marriage and Funeral Allowance

Marriage allowance shall be payable in advance, for once, at the amount of two years of pension or income they receive, upon marriage and request of the daughters, whose income or pensions should be terminated due to marriage.

In case a right holder who is receiving marriage allowance becomes right holder within two years following the termination date of the pension, no income or pension shall be payable until the end of two-year period however such individuals shall be deemed to be universal health insurance holders.

Funeral allowance shall be payable to the right holders of the insurance holder who deceased when receiving permanent incapacity income due to work accident or occupational disease, invalidity, duty disability or old - age pension or when minimum 360 days of invalidity, old - age and survivors insurance premiums are notified for himself/herself.

Main Page

- Minister

- Introduction of the President of Institution

- Objectives and Duties of SSI

- History

- Organization Chart

- Social Security System

- Short Term Insurance Branches

- Long Term Insurance Branches

- Universal Health Insurance

- E-book on Universal Health Insurance System in Turkey

- E-book on the Organizational Profile of SGK & Social Security System in Turkey

- I Want To Make Crediting For My Foreign Services

- Foreign Pension Transactions

- Social Security Agreements

- Foreign Healthcare Transactions

- Social Security Rights in the Process of Membership to European Union

- On-going Projects and Activities Made During the Process of Social Security Reform

- ISSA (International Social Security Association)

- Statistics

- Basic Indicators of Monthly Social Security

- Monthly Statistical Information

- Monthly Statistical Bulletins

- Useful Links

- Contact Us

Web Content Viewer Footer SGK

Actions

- ${title}